Reverse Charge Mechanism

Under Normal Scenario, tax is paid by a supplier who makes a supply of goods or services or both. However, under Reverse Charge Mechanism, liability to pay tax would not be on the supplier of goods or services or both but on the recipient of such goods or services or both.

Some of the reasons for the levy of tax under reverse charge mechanism wherein the person receiving the goods or services is liable to pay tax are as follows:

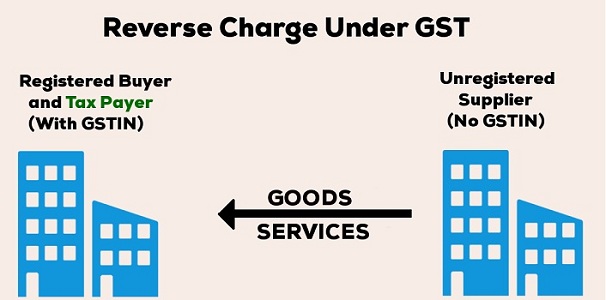

- Supplier of the goods or services is unregistered and he makes supply of goods or services to a registered person:

- A multi-point tax system helps creating a trail of the transaction from the start of the supply chain to the endpoint of the supply chain. However, if an unregistered person supplies goods or services or both to a registered person, he breaks the trail of the supply chain as he would not be filing any return declaring the details of the person from whom he has received goods or services or both and person to whom he has supplied goods or services.

- Therefore, the law requires the registered person to pay tax on such supply received from unregistered person to pay tax on such supply received from unregistered person and avail the credit of the taxes paid, had he received the goods or services from a registered person.

Reverse Charge Mechanism in GST

- Supplier of the goods or services or both located in non-taxable territory:

- GST is destination-based taxation. Therefore, if the supplier is located in a non-taxable territory and cannot collect and deposit taxes from the recipient then the recipient himself is made liable to deposit tax under reverse charge mechanism. This helps similar levels of taxes on goods or services whether they are imported from outside the taxable territory or produced/ rendered within the taxable territory. Therefore, there is no benefit on the goods or services imported from outside the taxable territory on account of a lower rate of taxes.

- Tax is levied under Reverse Charge Mechanism on an unorganized sector:

- Sometimes, taxes are levied on reverse charge basis on certain goods or services or both wherein many people fall under the unorganized sector. The cost of administering and collecting tax from such local or unorganized sector would be too high. Sometimes, it could also be that the persons working in the sector might be many but their aggregate turnover is less. Under these circumstances, it would not be possible for each of them to be registered under the law as the majority here would be below the threshold limit of aggregate turnover. Therefore, in such cases, if the goods or services supplied by persons in an unorganized sector happens to be a B2B Supply, then law might provide levy of tax on reverse charge basis on the business which is receiving goods or services or both from such source.

- Indirect Levy of tax on a sector which is generally exempt from tax:

- Legislature may exempt specific goods or services or both from levy of the tax but indirectly tax is levied on that sector under reverse charge mechanism whereby the recipient of such goods or services or both has to deposit tax.

Person would be liable to pay tax under reverse charge under two categories:

- Category of suppliers of goods or service or both notified by the Government:

- Government may, on the recommendation of the Council, would notify categories of supplies of goods or services or both on which tax would be payable on reverse charge basis. The Liability to pay tax on the goods or services notified under the reverse charge mechanism would be on the recipient of goods or services or both and he would be treated as the person liable to pay tax on such goods or services or both. Supplier of goods or services or both would not be the person liable to pay tax on such supplies.

- Supply of Taxable Goods or Service or both by an unregistered person to a registered person:

- Wherein any supply of goods or services or both is made by a supplier who is not registered to a registered person, then tax in respect of such supply of taxable goods or services or both shall be paid by the registered person on reverse charge basis. That such registered person shall be treated as the person liable for paying tax in relation to the supply of such goods or services or both. Registered person would now be bound to receive supply of taxable goods or services or both from a registered supplier only and in case he receives a taxable supply of goods or services from an unregistered supplier, then in all such cases registered person would be liable to pay tax on reverse charge basis. This would be an onerous task upon the registered person to monitor that all taxable supplies of goods or services or both are received from registered persons only.