Reverse Charge Mechanism

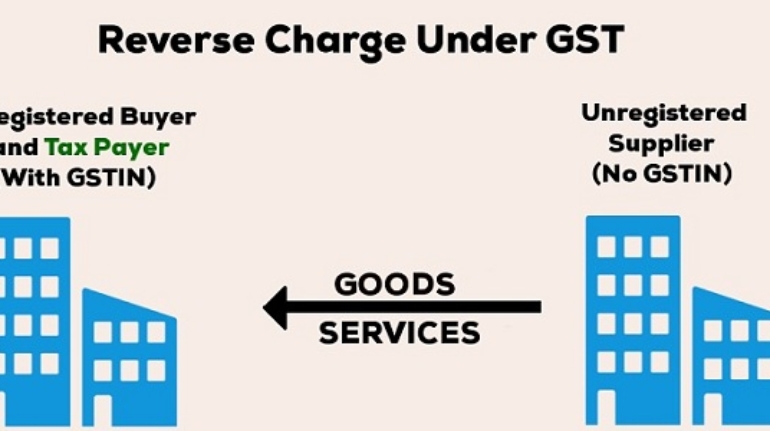

Reverse Charge Mechanism Under Normal Scenario, tax is paid by a supplier who makes a supply of goods or services or both. However, under Reverse Charge Mechanism, liability to pay tax would not be on the supplier of goods or services or both but on the recipient of such goods or services or both. Some of the reasons for the levy of tax under reverse charge mechanism wherein the person receiving the goods or services is liable to pay tax are as follows: Supplier of the goods or servic ...