Financial Instruments

The objective of this Indian Accounting Standard is to establish principles for the financial reporting of financial assets and financial liabilities that will present relevant and useful information to users of financial statements. IND AS 109 Financial Instruments deals with classification, recognition, de-recognition and measurement requirements for all the financial assets and liabilities.

Definition

A financial instrument is any contract that gives rise to – a financial asset of one entity and a financial liability or equity instrument of another entity. An asset that is:

Cash

An equity instrument of another entity

A contractual right

- To receive cash or another financial asset; or

- To exchange financial assets or financial liabilities under potentially favorable conditions; or

A contract that will or may be settled in the entity’s own equity instruments and is A non-derivative for which the entity is or may be obliged to receive a variable number of the entity’s own equity instruments; or A derivative that will or may be settled other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of the entity’s own equity instruments A financial liability is any liability that is : A contractual obligation :

- To deliver cash or another financial asset to another entity or

- To exchange financial assets or financial liabilities with another entity under conditions that are potentially unfavorable to the entity or

- A contract that will or may be settled in the entity’s own equity instruments and

A non-derivative for which the entity is or may be obliged to deliver a variable number of the entity’s own equity instruments; or A derivative that will or may be settled other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of the entity’s own equity instruments. An equity instrument is any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities. Fair value is the amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm’s length transaction. A puttable instrument is a financial instrument that gives the holder the right to put the instrument back to the issuer for cash or another financial asset or is automatically put back to the issuer on the occurrence of an uncertain future event or the death or retirement of the instrument holder.

Classification

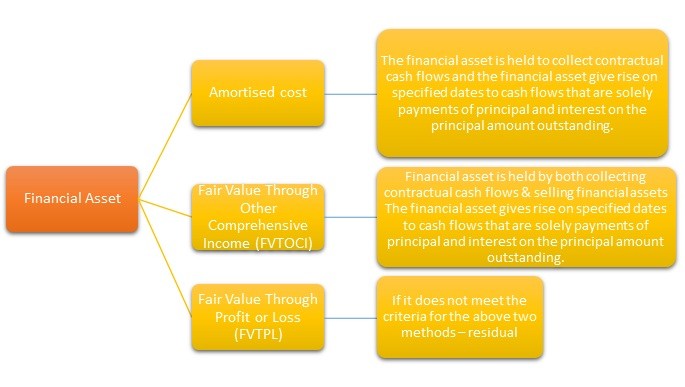

Debt Instruments

If the Financial asset is debt instrument, the management should consider the following assessments in determining its classification: a. The entity’s business model for managing the entity. b. The contractual cash flows characteristics of an asset.

Recognition

Initial Recognition – An entity shall recognize a financial asset or a financial liability in its balance sheet when, and only when, the entity becomes party to the contractual provisions of the instrument. Subsequent Recognition – A regular way purchase or sale of financial assets shall be recognized and derecognized, as applicable, using trade date accounting or settlement date accounting.

Derecognition

Financial Assets:

a. In consolidated financial statements, this concept is applied at a consolidated level. Hence, an entity first consolidates all subsidiaries in accordance with Ind AS110 and then applies de-recognition to the resulting group subject to certain conditions. b. An entity shall de-recognize a financial asset only i. When the contractual rights to the cash flows from the financial asset expire, or ii. It transfers the financial asset and the transfer qualifies for derecognition. c. An entity transfers a financial asset if, and only if, it either: i. Transfers the contractual rights to receive the cash flows of the financial asset, or ii. Retains the contractual rights to receive the cash flows of the financial asset, but assumes a contractual obligation to pay the cash flows to one or more recipients in an arrangement that meets the conditions. d. When an entity retains the contractual rights to receive the cash flows of a financial asset (the ‘original asset’), but assumes a contractual obligation to pay those cash flows to one or more entities (the ‘eventual recipients’), the entity treats the transaction as a transfer of a financial asset if, and only if, all of the following three conditions are met. i. The entity has no obligation to pay amounts to the eventual recipients unless it collects equivalent amounts from the original asset. Short-term advances by the entity with the right of full recovery of the amount lent plus accrued interest at market rates do not violate this condition. ii. The entity is prohibited by the terms of the transfer contract from selling or pledging the original asset other than as security to the eventual recipients for the obligation to pay them cash flows. iii. The entity has an obligation to remit any cash flows it collects on behalf of the eventual recipients without material delay. In addition, the entity is not entitled to reinvest such cash flows, except for investments in cash or cash equivalents (as defined in Ind AS 7 Statement of Cash Flows) during the short settlement period from the collection date to the date of required remittance to the eventual recipients, and interest earned on such investments is passed to the eventual recipients.

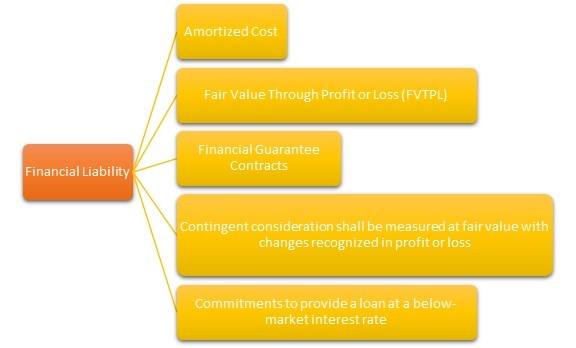

Financial Liabilities

a. An entity shall remove a financial liability (or a part of a financial liability) only when it is extinguished (Contract obligation is discharged or canceled or expires). b. An exchange between an existing borrower and lender of debt instruments with substantially different terms shall be accounted for as an extinguishment of the original financial liability and the recognition of a new financial liability. Similarly, a substantial modification of the terms of an existing financial liability or a part of it (whether or not attributable to the financial difficulty of the debtor) shall be accounted for as an extinguishment of the original financial liability and the recognition of a new financial liability. c. The difference between the carrying amount of a financial liability (or part of a financial liability) extinguished or transferred to another party and the consideration paid, including any non-cash assets transferred or liabilities assumed, shall be recognized in profit or loss. d. If an entity repurchases a part of a financial liability, the entity shall allocate the previous carrying amount of the financial liability between the part that continues to be recognized and the part that is derecognized based on the relative fair values of those parts on the date of the repurchase. The difference between (a) the carrying amount allocated to the part derecognized and (b) the consideration paid, including any non-cash assets transferred or liabilities assumed, for the part derecognized shall be recognized in profit or loss.

Embedded derivatives

1. An embedded derivative is a component of a hybrid contract that also includes a non-derivative host contract. Some of the cash flows of the combined instrument vary in a way similar to a stand-alone derivative. 2. A derivative that is attached to an FI but is contractually transferable independently of that instrument, or has a different counterparty, is not an embedded derivative, but a separate FI. Impairment- Financial instruments: 1. Applicability:- i. Debt instruments measured at amortized cost ii. Debt instruments measured at fair value through other comprehensive income iii. Loan commitments and financial guarantee contracts not measured at fair value through profit or loss iv. Trade receivables and contract assets v. Lease receivables. 2. Expected credit loss model: i. According to the simplified approach, for trade receivables and contract assets that do not contain a significant financing component, an entity shall always measure loss allowance at an amount equal to lifetime expected credit losses. ii. A provision matrix could be used to estimate ECL for these financial instruments. 3. Determining significant increases in credit risk i. At each reporting date, an entity shall assess whether the credit risk on a financial instrument has increased significantly since initial recognition. When making the assessment, an entity shall use the change in the risk of a default occurring over the expected life of the financial instrument instead of the change in the amount of expected credit losses. To make that assessment, an entity shall compare the risk of a default occurring on the financial instrument as at the reporting date with the risk of a default occurring on the financial instrument as at the date of initial recognition and consider reasonable and supportable information, that is available without undue cost or effort, that is indicative of significant increases in credit risk since initial recognition. ii. An entity may assume that the credit risk on a financial instrument has not increased significantly since initial recognition if the financial instrument is determined to have low credit risk at the reporting date. iii. If reasonable and supportable forward-looking information is available without undue cost or effort, an entity cannot rely solely on past due information when determining whether credit risk has increased significantly since initial recognition. However, when information that is more forward-looking than past due status (either on an individual or a collective basis) is not available without undue cost or effort, an entity may use past-due information to determine whether there have been significant increases in credit risk since initial recognition. Regardless of the way in which an entity assesses significant increases in credit risk. Write-off: Gross Carrying Amount of a financial asset is directly reduced when no reasonable expectations of recovering a financial asset in its entirety or a portion thereof. Hybrid contracts with financial asset hosts: A hybrid contract contains both derivative and non- derivative which is not possible to transfer independent of the host contract. If a hybrid contract contains a host that is not an asset, an embedded derivative shall be separated from the host and accounted for as a derivative only if: (a) The economic characteristics and risks of the embedded derivative are not closely related to the host. (b) If an embedded derivative is separated, the host contract shall be accounted for in accordance with the appropriate Standards. This Standard does not address whether an embedded derivative shall be presented separately in the balance sheet. (c) The hybrid contract is not measured at fair value with changes in fair value recognized in profit or loss. If unable to separate and measure embedded derivative from its host either, then designate the entire hybrid contract as at FVTPL. If an entity is unable to measure reliably the fair value of an embedded derivative on the basis of its terms and conditions, the fair value of the embedded derivative is the difference between the fair value of the hybrid contract and the fair value of the host. Hedging Accounting (HA): Application of hedge accounting permits to: 1. Remeasure both the items from which the risk exposure arises and the instruments used to manage the risk in profit or loss; or 2. Defer recognition in profit or loss of certain gains and losses on derivatives by recognizing them in OCI. A hedged item is remeasurement to fair value in respect of hedged risk recognized in profit or loss. The hedged item can be a single item or a group of items which are reliably measurable or probable. A hedging relationship qualifies for hedge accounting only if all of the following criteria are met: (a) It consists only of eligible HI and eligible hedged item (b) There are formal designation and documentation and the entity’s risk management objective (c) Meets all of the following hedge effectiveness requirements: a. Economic relationship between the hedged item and HI b. The effect of credit risk does not dominate the value changes and c. The hedge ratio of the hedging relationship is the same as that the entity actually hedges and the quantity of the HI that the entity actually uses to hedge that quantity of hedged item

Type of Hedges:

1. Fair Value Hedge 2. Cash flow Hedge 3. Net Investment Hedge Accounting treatment for the three types of hedging relationships: A. Fair value hedge: 1. The gain or loss on the HI recognized in profit or loss 2. Hedging gain or loss on the hedged item is adjusted to the GCA. Gain or loss of financial asset measured at FVTCI is recognized in profit or loss 3. Hedged item is an equity instrument adopting changes in FVOCI shall remain in OCI 4. Hedged item is an unrecognized firm commitment, the cumulative change in the fair value is recognized as an asset or a liability with a corresponding gain or loss recognized in P&L B. Cash flow hedge: 1. Cash flow hedge reserve is adjusted to the lower of the following: (i) The cumulative gain or loss on the HI from its inception (ii) The cumulative change in fair value of the HI 2. The portion of the gain or loss on the HI that is determined to be an effective hedge is recognized in OCI. 3. Any remaining gain or loss on the HI is hedge ineffectiveness is recognized in P&L C. Net Investment Hedge: 1. Portion of the gain or loss on the HI that is determined to be an effective hedge is recognized in OCI 2. An ineffective portion is recognized in P&L. Compound instruments: 1. The issuer of a non-derivative financial instrument shall evaluate the terms of the financial instrument to determine whether it contains both a liability and an equity instrument. 2. Such components shall be classified separately as financial liabilities, financial assets or equity instruments. Reclassification: An entity is required to reclassify financial assets when it changes its business models for managing financial assets. Investment in equity instruments that are designated as at FVTOCI at initial recognition cannot be reclassified, since, the election to designate as at FVTOCI is irrecoverable. Reclassifications are to be expected to be very infrequent. Such changes must be determined by the entity’s senior management as a result of external or internal changes in an entity’s operations and demonstrable to external parties. When an entity changes its business model for managing financial assets then reclassify all affected financial assets. An entity cannot reclassify any financial liability. Classification is done based on certain principles, hence reclassification to be done if principles changes. Measurement has to be done on the date of reclassification. Measurement of Reclassification

| Initial | Revised | Accounting |

| Amortized Cost | FVTPL | FV on reclassification date and difference in PL |

| Amortized Cost | FVOCI | FV on reclassification date and difference in OCI |

| FVOCI | Amortized Cost | FV on reclassification date is carrying value. Cumulative gain/loss in OCI adjusted to FV |

| FVOCI | FVTPL | Asset considered at FV. Cumulative gain/loss in OCI adjusted in PL |

| FVTPL | FVOCI | Asset considered at FV |

| FVTPL | Amortized Cost | FV on reclassification date is carrying value. New EIR computed |