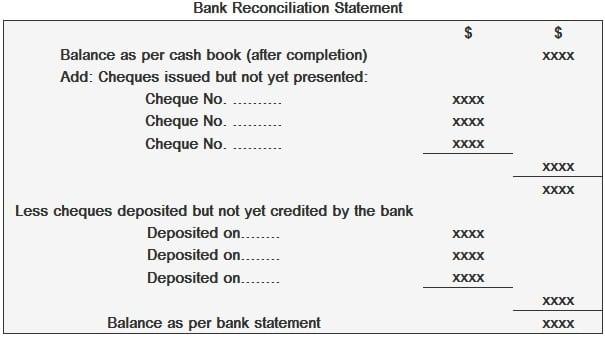

Bank Reconciliation Statement

A bank reconciliation statement is a summary of banking and business activity that reconciles an entity’s bank account with its financial records. The statement outlines the deposits, withdrawals and other activity affecting a bank account for a specific period. A bank reconciliation statement is a useful financial internal control tool used to thwart fraud. A Bank reconciliation statement is a statement prepared as part of the reconciliation which sets out the entries which have caused the difference between the two balances. It‘s not compulsory to prepare a BRS and there’s no fixed date for preparing BRS. BRS is prepared on a periodical basis for checking that bank related transactions are recorded properly in cash book’s bank column and also by the bank in their books. BRS helps to detect errors in recording transactions and determining the exact bank balance as on a specified date.

Reasons for Difference:

When banks send companies a bank statement that contains the company’s beginning cash balance, transactions during the period, and ending cash balance, almost always the bank’s ending cash balance and the company’s ending cash balance are not the same. Some reasons for the difference are:

Deposits in transit: Cash and checks that have been received and recorded by the company but have not yet been recorded on the bank statement.

Outstanding checks: Checks that have been issued by the company to creditors but the payments have not yet been processed.

Bank service fees: Banks deduct charges for services they provide to customers but these amounts are usually relatively small.

Interest income: Banks pay interest on some bank accounts.

Not sufficient funds (NSF) checks: When a customer deposits a check into an account but the account of the issuer of the check has an insufficient amount to pay the check, the bank deducts from the customer’s account the check that was previously credited. The check is then returned to the depositor as an NSF check.

Nowadays, many companies use specialized accounting software in bank reconciliation to reduce the amount of work and adjustments required and to enable real-time updates.

Process of preparing BRS:

- The first step is to compare opening balances of both the bank column of the cash book as well as bank statement; these could be different due to un-credited or un-presented cheques from a previous period.

- Now, compare the credit side of the bank statement with the debit side of the bank column of the cash book and debit side of the bank statement with the credit side of the bank column of the cash book. Place a tick against all the items appearing in both the records.

- Analyze the entries both in the bank column of the cash book as well as passbook and look for entries which have been missed to be posted in the bank column of the cash book. Make a list of such entries and make the necessary adjustments in the cash book.

- Correct if any mistakes or errors appear in the cash book.

- Calculate the corrected and revised balance of cash book’s bank column.

- Now, start a bank reconciliation statement with an updated cash book balance.

- Add the un-presented cheques (cheques which are issued by the business firm to its creditors or suppliers but not presented for payment – Expense) and deduct un-credited cheques (Cheques paid into the bank but not yet collected – Income).

- Make all the necessary adjustments for the bank errors. In case the bank reconciliation statement begins with the debit balance as per the bank column of the cash book, add all the amounts erroneously credited by the bank and deduct all the amounts erroneously credited by the bank. Do vice-versa in case it start with the credit balance.

- The resultant figure must be equal to the balance as per the bank statement.

BRS proves to be a useful tool in fixing irrelevant faults in bank statements. Bank statements are useful in huge transactions and in making Income Tax Return (ITR) statements. We can call it a basic medium of operation in banking. If basic is not justified, unidentified problems arise with further documents.

Reconciliation makes the bank statement error-free and clears additional charges. Therefore, before closing the accounting chapter in the banking book, reconciliation checks whether the closing page hits green light i.e. ending is correct and safe.