GST Registration

GST Registration compliance

GST Registration is done by every supplier who is making a taxable supply of goods or services or both shall register in every State/Union Territory from where he makes taxable supply if his aggregate turnover exceeds 40 lakhs (10 lakhs for northeastern states) in a financial year.

Aggregate turnover means the value of all taxable supplies (excluding the value of inward supplies liable to tax on reverse charge basis), exempt supplies, exports of goods and services or both and inter-state supplies of persons having the same Permanent Account Number [PAN] to be computed on all India basis.

Mandatory GST Registration Criteria

The following person is required to take registration under GST irrespective of turnover:

- Person making interstate supplies

- casual taxable persons

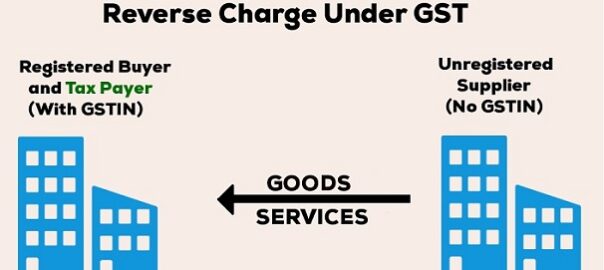

- Persons who are required to pay tax under RCM

- Person who are required to pay tax under sub-section (5) of section 9

- Non-resident taxable persons making taxable supply

- Persons who are required to deduct tax under section 51

- Persons who make taxable supply of goods or services or both on behalf of other taxable persons whether as an agent or otherwise

- Input Service Distributor

- Persons who supply goods or services or both, other than supplies specified under sub-section (5) of section 9, through such electronic commerce operator who is required to collect tax at source under section 52

- Every E-commerce operator

- Every person supplying OIDR services from a place outside India to a person in India, other than a registered person.

Composition Scheme:

Small businesses having an annual turnover of less than Rs. 1.5 crore can opt for Composition scheme

Composition dealers will pay nominal tax rates based on the type of business:

- Composition dealers are required to file only one quarterly return (instead of three monthly returns filed by normal taxpayers).

- They cannot issue taxable invoices, i.e., collect tax from customers and are required to pay the tax out of their own pocket.

- Businesses that have opted for Composition Scheme cannot claim any input tax credit.

Composition scheme is not applicable to :

- Service providers

- Inter-state sellers

- E-commerce sellers

- Supplier of non-taxable goods

- Manufacturer of Notified Goods

Input Service Distributor:

ISD means Input Service Distributor. It is like a head office that receives the tax invoices of input services and then further distributes the credit of tax paid by it to its units proportionately.

- Yes, the person can voluntarily cancel the registration on wish.

- Even proper office, on default of tax by taxable assessee, will cancel the GST registration by giving notice.

Documents Required:

- PAN of the applicant & Valid Mobile Number and E-Mail ID

- Identity PAN and address proof along with photographs of promoter

- Proprietary Concern – Proprietor

- Partnership Firm / LLP – Managing/Authorized/Designated Partners (personal details of all partners are to be submitted but photos of only ten partners including that of Managing Partner are to be submitted)

- Hindu Undivided Family – Karta

- Company – Managing Director, Directors and the Authorised Person

- Trust – Managing Trustee, Trustees and Authorised Person

- Association of Persons or Body of Individuals –Members of Managing Committee (personal details of all members are to be submitted but photos of only ten members including that of Chairman are to be submitted)

- Local Authority – CEO or his equivalent

- Statutory Body – CEO or his equivalent

- Others – Person(s) in Charge

- Business Registration Document

- Partnership – Partnership Deed

- LLP/ Company – Incorporation Certificate

- Society/trust/ club/ government department/ body of individuals – Registration Certificates

- Address proof of business

- Rental – Rental Agreement/ Electricity Bill with Consent

- Own – Property tax/ Municipal tax receipt

- SEZ – Certificate issued by Govt.

- Jurisdiction and Commissionerate

- Bank account Proof

- Cheque

- Bank statement

- Digital Signature Mandatory only in case of Company

- Declaration as authorized signatory – Board Resolution/Self Declaration

- Declaration regarding the type of goods and nature of business.