Income Tax Filling Package

-

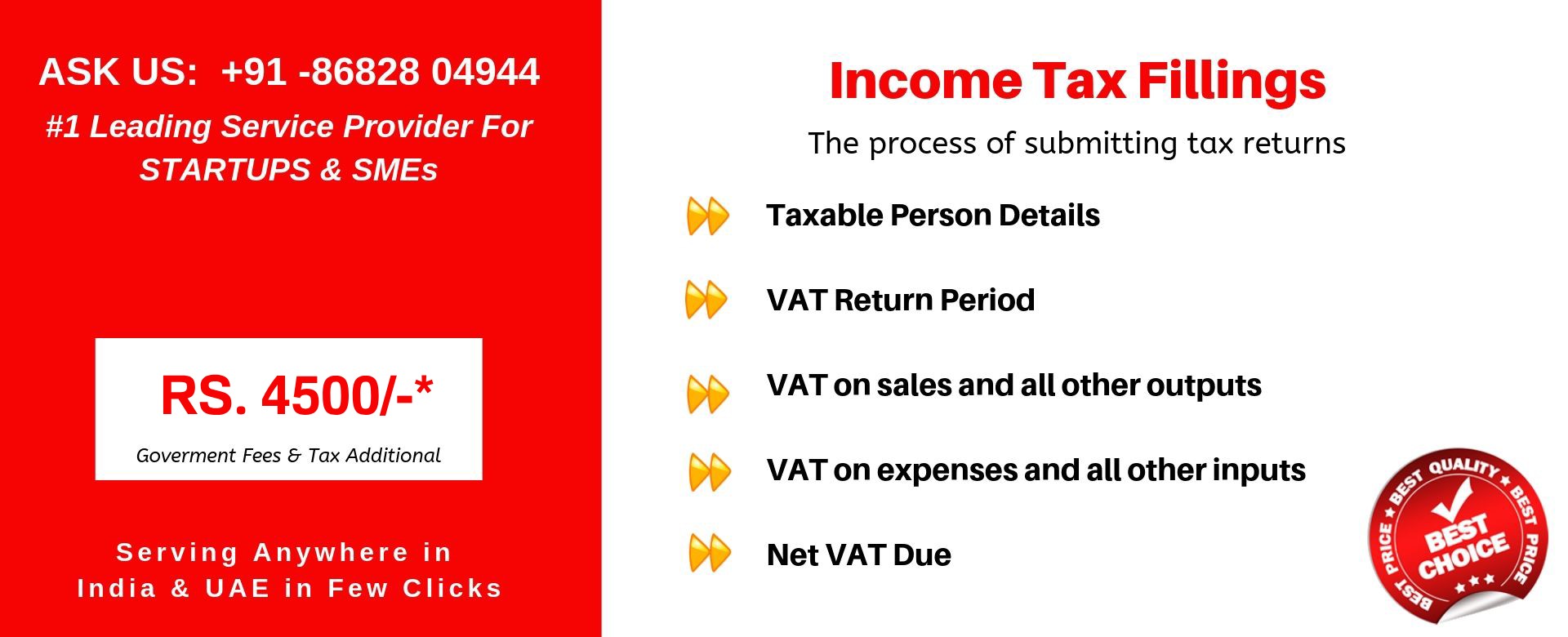

Income Tax E-Filing

-

Rs2899

-

Register to e-file ITR

-

Details filled up

-

Verification of PAN

-

Activation of Account

Income tax e-filing in india

Documents required for income tax return e filing in india

1. Form 16 / Payslips ( for salaried employee )

2. Financial Data / Tally data ( if available ) - Income from Business/ Profession

3. List of Expenditure spent on LIC, House Loan, Medical etc.

4. List of Donations given

5. Bank Statement

6. Form 26AS

7. Investment Declaration

Slab for the Assessment Year 2020-21 Individual - income tax e-filing in india

| Income Less than 5 Lakhs | No tax |

| If Income Greater than 5 Lakhs then | |

| Up to 2.5 Lakhs | Nil |

| 2.5 Lakhs to 5 Lakhs | 5% |

| 5 Lakhs to 10 Lakhs | 20% |

| Above 10 Lakhs | 30% |

| Partnership | Flat 30% |

| Domestic Company | Flat 25% |

| Foreign Company | Flat 40% |